The Day the

“Blueback” Goes Live

This dollar replacement day will have Americans

standing in long lines at their local banks, literally screaming for the right to withdraw their hard-earned money. Read on before the curtain closes on the greenback as you know it...

Dear Fellow American:

It’s 7:00 AM.

You roll out of bed, thinking today will be like every other day.

But you’re about to be very wrong.

Instantly, you hear police sirens wailing down the main road of your town…

As you move to the window, you a see motorcade of patrol cars and ten armored Brink’s trucks fly down the street…

They’re easily 30 mph over the speed limit…

And they're headed to your local bank...

The same bank where you cash and deposit your checks.

You race to the TV to find out what’s happening.

You tune in to your local news station to watch the historic moment on live television.

The armored trucks pull into your bank’s parking lot.

The screen on the TV reads: “BREAKING NEWS: NEW BLUE DOLLAR GOING INTO EFFECT, CHAOS ENSUES.”

Crowds are standing around with their cellphones out...

They’re recording what’s happening.

The police are making sure the protesters stay behind the barricades, but the crowds are growing restless…

They’re starting to push their way past the roadblocks and near the ATMs.

Police in riot gear hold shields. They demand peace and calm over the megaphones.

For a moment you forget how quickly it all happened…

The announcement had only been made by the president in an emergency briefing just ten days ago.

The backs of the armored trucks swing open…

And a massive pallet of bright blue, shrink-wrapped money is taken out.

The fronts of the ATMs are opened…

The old greenbacks you’ve always known are removed…

And the strange, crisp blue bills are inserted.

The ATM slams shut…

A protestor knocks down the barricade and begins to rush the bank…

A second shortly follows…

The police arm up, warning the crowd to fall back in line.

But like floodgates that open, protests spill from the street… over the barricades… and flood into the bank.

The first sprays of mace are fired into the crowd…

Hi, my name is Jim Rickards — please hold this startling image in your head for a moment...

I’m an American lawyer, economist, best-selling author and trusted financial threat advisor to the U.S. government…

And while for the moment, the scenario I’ve outlined is a cautionary tale…

It’s important to know two things…

- What you’re about to see isn’t some sci-fi script.

In fact, our country has made massive changes to our currency exactly NINE times before.

Changes just like the one I described for you.

And… - I’m not some wacko conspiracy theorist that lacks proof.

In my hands, right now, I have a copy of the 36-page paper proposing this new and strange era for Americans' cash...

And in the next 30 seconds I’m going to reveal a very real, but secret, proposal to destroy the current U.S. dollar in circulation…

And launch a brand-new physical American currency, which here and now I’m calling the “Blueback.”

This move would catch most Americans totally off guard, holding worthless dollars.

The ones in your wallet right now.

And if the scenario I’ve just outlined occurs...

Stores you shop at for groceries… clothes… medicine… the gas station where you fill up your tank... will no longer take your greenbacks.

Your financial privacy — what you buy, from whom and for how much — will be gone for good…

The government will soon track everything you buy.

They will know every move you make.

Hundreds of banks and insurance companies could shut their doors...

Gold and silver could become unattainable at any price.

And the U.S. dollar could cease to be the world’s #1 currency for trade, finance and savings.

Now, I know plenty of financial gurus have been making similar types of predictions for years.

But right here in this letter, I’m going to show you something none of them has ever shown you before.

I’m going to show you EXACTLY what’s going to replace the dollar as you know it...

And I’ll tell you the timeline it could all unfold in.

You need to take five simple — but crucial — steps with your money right now. Don’t wait another minute.

Because following my instructions today is not only the best way to protect yourself during the coming crash…

But mint yourself one of the “New Elites” in the coming new financial order.

Someone who has financial independence, peace of mind, and the respect of your peers and neighbors.

These are some of the same moves I’m making with over $1,000,000 of my own money.

Now, before I show you what the dollar’s replacement is...

Let me be clear about what this new “Blueback” dollar is NOT…

- >> It's NOT gold, silver or any precious metal...

- >> Not bitcoin...

- >> Not any paper currency in existence today...

- >> Not any commodity like oil, iron, copper, wheat…

- >> And not anything else you’re familiar with or have ever heard of.

Instead it's a new (and frightening) chapter in U.S. financial history.

Something not one in 100,000 people knows about.

It’s only through my deep government contacts… and ten years of intense economic and historical research... that I’ve uncovered this early information for you.

But the window to prepare for these new dollars is closing fast.

It’s not my intention to pressure you. Not at all...

But the cold truth is: When the global financial elites see what I’m sharing with you right now… they'll likely censor this information in a second’s notice.

That could happen by morning.

At that point, your hard-earned money could lose its value… and make you poorer and less free.

It will be too late. And I don’t want you to miss out.

Everything you need is here in this short letter.

But first, bold claims require bold backup...

Who am I?

Why should you listen to me?

And what gives me the right to talk about something so “out there” as a new, different-colored dollar changing your way of life?

Let me show you...

“Our Man in the Field...”

Sure, I’ve got all the “normal” credibility you hear from people that issue similar-sounding warnings…

I’m the author of two New York Times best-selling books — Currency Wars and The Death of Money — warning about the coming collapse of our financial system…

As well as the best-selling modern-day authority on the importance of gold in today’s monetary system, The New Case for Gold…

I have a high profile on popular financial TV, print and online media outlets…

Turn on the TV and tune into CNBC, Fox, Bloomberg or Russia Today and you’ll likely see me on the channel.

But that’s where my similarities with my peers end.

Because my credibility reaches far, far deeper than anyone else you know…

My work as a currency war advisor for the Pentagon, CIA and national intelligence brings me into direct contact with the top echelons of the U.S. power structure.

They’ve given me a top secret national security clearance, too.

I’ve testified in front of Congress...

I’ve sat deep in the Treasury Department… stared officials in the face and warned them about crises like 2008 years before it happened. (They ignored me…)

And while I can’t be specific with senior military or politicians’ names or statements, I can tell you they’re preparing for something big.

In one of my most high-profile missions, I helped senior U.S. military strategists at America’s Warfare Analysis Laboratory conduct their first-ever “financial war game” to determine threats against the U.S. dollar.

I routinely rub elbows with Federal Reserve board chairs like Ben Bernanke… five-star generals and NSA directors like Michael Hayden, finance ministers of various governments… presidents… prime ministers... Fortune 500 CEOs... and the world’s most powerful investment bankers.

They ask me for my opinions and tell me things they’ll never say publicly.

I’m not saying any of this to toot my own horn.

I’m only trying to give you my credentials so that you understand I’m much, much different from a newsletter desk jockey.

I want you to take my dire warning today seriously…

And realize that I’m in a unique position to help you.

You’re well within your rights to disagree with my analysis and conclusions.

All I ask is that you listen to what I have to say over the next few minutes.

It costs you nothing. And at the end, if you decide that I’m full of it, then you can ignore what I have to say.

You won’t hurt my feelings. But if I’m right…

You’ll have learned everything you need to protect your wealth and family when this new “Blueback” replaces our green money and forever changes the U.S.

I won’t waste any time. As a lawyer, I like evidence that proves a claim beyond any reasonable doubt.

And I have a copy of the paper proposing this new and strange era for Americans' cash...

Smoking Gun Proof the

“Blueback” Era Is on the Way

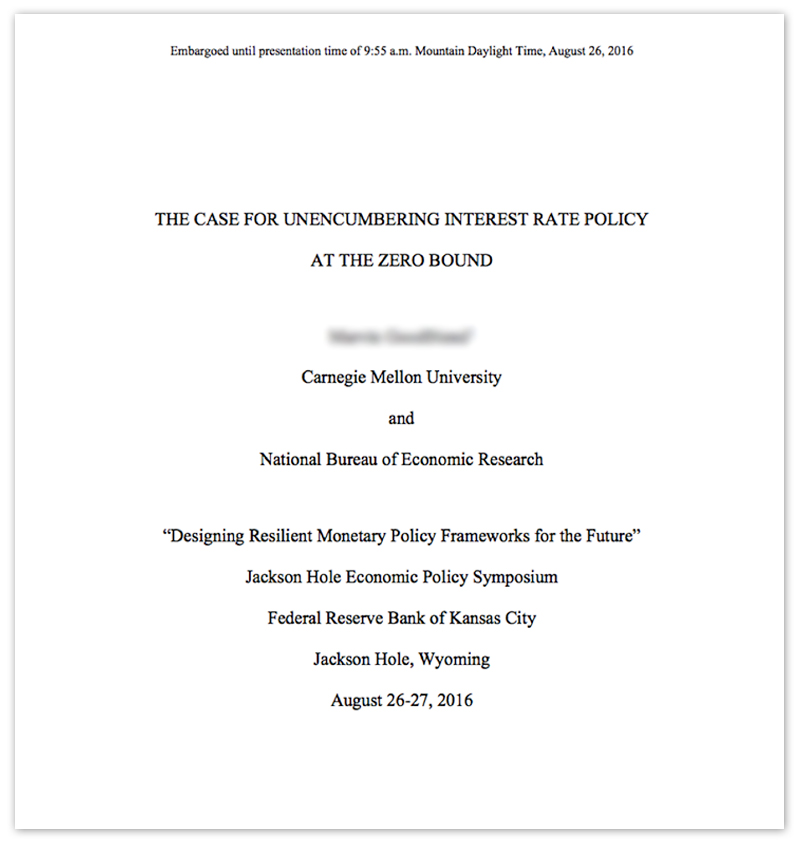

Every year, the world’s central bankers come together in Jackson Hole, Wyoming…

It’s an opportunity to make presentations about the future of money… banking… and central bank policy.

Often, the papers presented are technical and understandable only to the academics in attendance…

I call it “transparently hidden” information…

Meaning, it’s all publicly available… but impossible for an ordinary English speaker to comprehend.

But that’s what I do for a living…

And my jaw dropped after this year’s meeting on August 26, 2016, upon discovering thatone speaker for the National Bureau of Economic Research presented one particular paper.

The meeting’s theme was “Discussing Monetary Policy Frameworks for the Future.”

And the particular paper presented was obscurely titled: “The Case for Unencumbering Interest Rate Policy at the Zero Bound.”

Sounds like a real snooze-fest. What do those words even mean, right?

But that’s my whole point. The paper is public… but no one is going to spend their free time reading it. We all have better things to do...

This is what I do on my Saturday nights, though…

Now, an official would never use the term “Blueback.” Not only would it be too shocking… but it would also be too understandable to Americans for their taste.

Instead, they used five words in this paper that smacked me right between the eyes when I read them.

They're what led me on my investigation and ultimately to write this warning about this new “Blueback.”

It was when this professor suggested the government introduce a “Flexible Deposit Price of Paper Currency.”

Remember these five words.

At first glance, this sentence seems harmless or overly technical…

But it means something sinister that leads right up to the “Blueback.”

You see, in this very same white paper, this professor explained that in order for the government to do its job, they would need to “abolish paper currency.”

That’s no more cash. No more bills in your wallet. No more ATMs. No more leaving tips on the table. No more $20 bills in your grandchild’s Christmas card.

But he knows that you and I wouldn’t like that very much…

He literally admitted:

“The public is likely to resist the abolition of paper currency”...

But instead of listening to you and me and calling it quits…

He revealed a sneaky proposal that would eliminate your cash anyway.

He said even though Americans would never allow the government to abolish cash right now, it would be easy to do if…

“ATM charges for access to paper currency become excessive, and/or electronic currency substitutes become widely available…”

What he meant is if it cost you a lot of money to withdraw cash from an ATM, you would eventually stop.

Then, after a while, when you got used to not using cash… it’d be easy to abolish it.

That could happen in three steps that I’ll explain to you right now.

This new “Blueback” is one of the key steps in that process...

But first, it’s important you understand WHY officials are even talking about eliminating cash in the first place...

Three Little Charts and the End of the Greenback

If you’ve been paying attention to financial news you might have heard about the government’s so-called “War on Cash.”

The elites in government and academia who wage this war on cash give three excuses why cash should be banned:

- >> Drug dealers, criminals and terrorists use cash to stay anonymous and fund their operations…

- >> Counterfeiters can make their own physical currency…

- >> Businesses can be “cash only” and avoid paying their fair share of taxes...

But those are not the REAL reasons for this war on cash…

The true reason is that the greatest financial crisis in history is about to slam America…

And the government doesn’t have enough money to bail out the system like they did in 2008.

- So they're going to steal YOUR money.

- And if you can withdraw and hide your money in cash… under your mattresses… in home safes... then they can’t steal it from you.

THAT’S why there’s a war on cash.

You only need to look at three charts to see the government’s problem clearly...

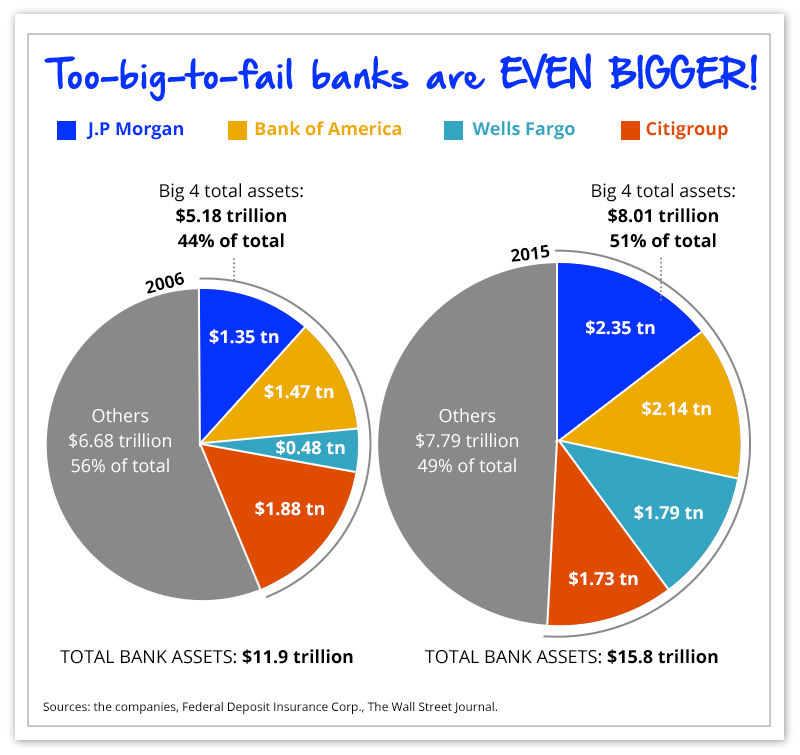

First, all of those “too-big-to-fail” banks that caused the 2008 crisis are 33% bigger today:

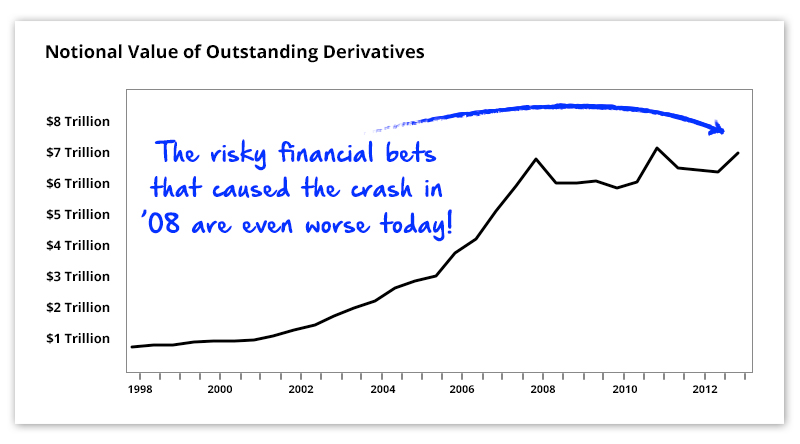

Second, all of the risky “derivative” bets the banks made that also went bad in 2008 are more numerous and riskier than ever before:

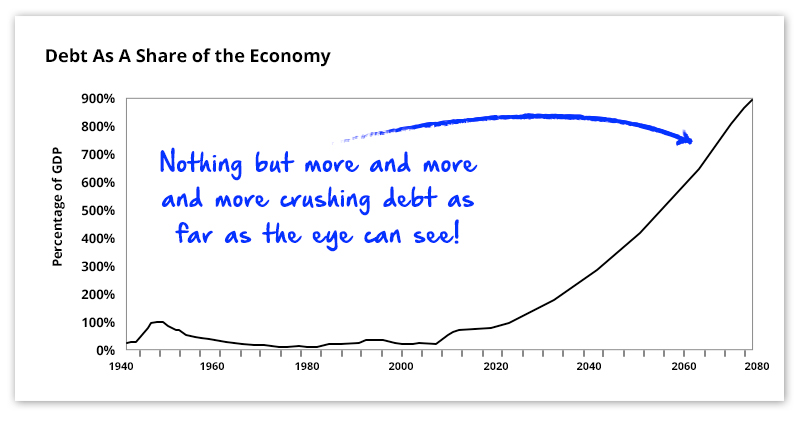

And third, since the 2008 crisis the combined debt has risen by $10 trillion… with the Office of Management and Budget and the Congressional Budget Office projecting the debt to become as much as 250% of GDP in the years ahead:

Everything that was a nightmare come true in 2008 could be about to return with a vengeance.

In 2008, the government launched a $700 billion stimulus program.

And the Federal Reserve printed over $3.5 trillion in new money and passed it out to their banker friends...

What is the government going to do next time the system collapses?

Spend $10 trillion or even $20 trillion to save the system?

No. They can’t.

Listen, as the government’s trusted financial threat advisor, I can tell you this with 100% certainty:

- *** I firmly believe the Treasury and the Federal Reserve are tapped out and have used all of their options.

Which brings us back to the government’s war on cash and this new “Blueback”...

The government may not have the money it needs to bail out the financial system.

But 300 million Americans DO have the money… collectively.

In your savings accounts… 401(k)s… in your brokerage accounts and money market funds… heck, even in your grandchildren's piggybanks!

When the government’s back is against the wall, nothing’s off limits.

According to the Federal Reserve, Americans’ total wealth equals $89.1 trillion.

That’s more than five times the national output of the U.S. every year.

It’s all of your money… all of my money… and all of our neighbors’ money… combined.

And it means one thing:

- We are, all of us, fattened calves.

- And the government wants to slaughter us… roast us… and feast on our juicy flesh.

To do that, they need one thing:

Complete, Total and Absolute Control Over You and Your Money

Any good beef cow farmer knows the first step to slaughtering his cattle is getting them all into one single pen.

And remember you and me are the beef cows.

But right now, we’re outside of “the pen.”

We’re able to withdraw our money… and keep it in cash...

We can come and go places as we please…

Transact with who we want…

Buy and sell the things we want….

Do it all anonymously, if we’d like…

We’re “free range.”

But that’s a big problem for the government.

And the government is the farmer in this story.

The pen they’ll force us into?

The banks.

And throughout history, when the government runs out of options to pay its debt or maintain social order… it resorts to complete control.

It needs the ability to control every citizen’s move… every cent they own… and every action they take.

That way it can manage crises and retain its power.

The alternative would be defaulting on its debt… or giving up its power…

And I think you know that a government giving up its power is like dry water… It just doesn’t exist.

The government debt… bad derivatives bets… and the bigness of the banks that made them is a ticking time bomb for the next crisis.

It could literally blow up any day now, and be ten times worse than the 2008 crisis.

And that’s why the government is preparing for total control over you, your money and everyone else in the economy.

That control is only possible if everyone in America and their wealth is in one place.

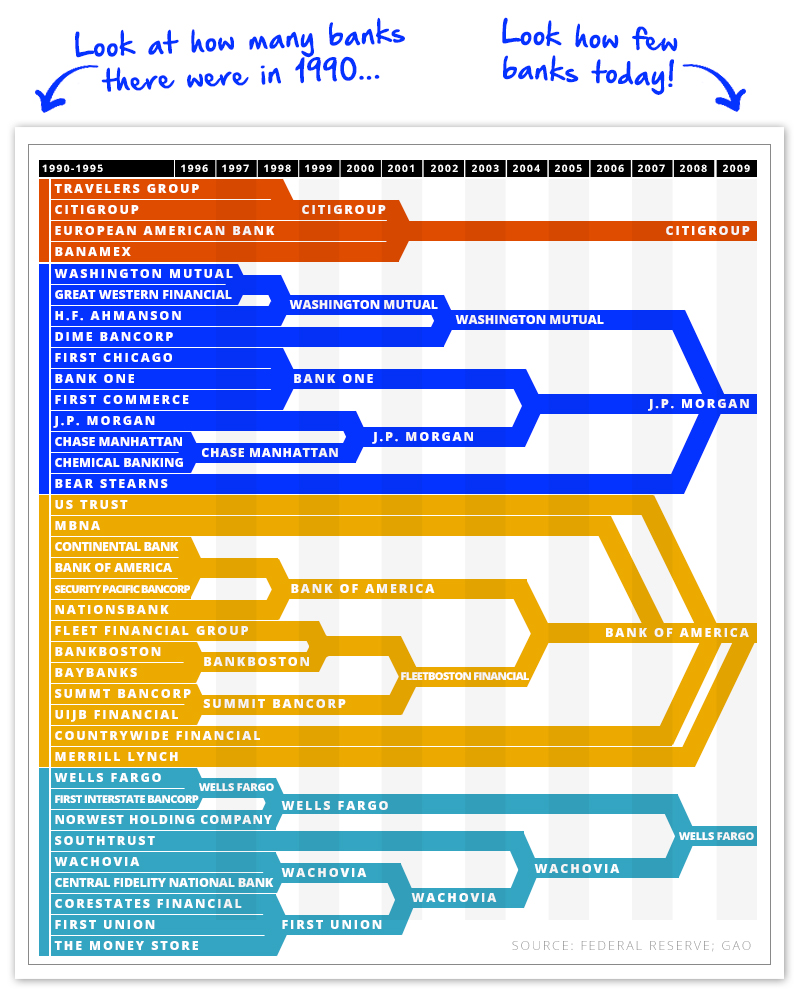

According to one report, there are fewer banks today in America than at any other time in U.S. history since the Great Depression.

Over time the government has helped them merge together until there were only a few mega-banks left.

And soon, they'll be a roach motel. You’ll have to check in, but you can never leave...

That way, the government will be able to track your every move… your transactions…

They'll be able to make you docile and obedient, for fear of punishment or wealth confiscation…

And they could steal some of everyone's wealth outright to pay their debts or prop up banks…

How? And when? And where does the “Blueback” I started this letter with come in?

Let’s take them in order.

There are three phases to this plan to round up everyone’s money… and steal your wealth.

It will all start with the stroke of a pen...

PHASE 1: Executive Order “6012-2” Is Signed

On a seemingly random day, the president would go live on TV, and announce that he’s signed a special executive order to launch a new type of currency.

The announcement would have two major parts...

- — All Americans would need to deposit their greenbacks at their local bank branch under pain of imprisonment, heavy wealth confiscation or both.

- — After the deadline, a new paper currency will be launched...

This will be Executive Order “6012-2.”

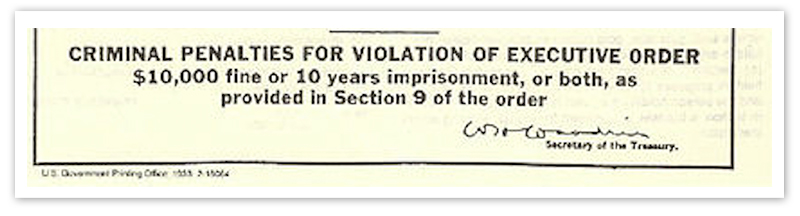

That’s because on April 5, 1933, President Franklin Roosevelt signed executive order 6012 to confiscate Americans’ gold.

Everyone was forced to turn in their physical gold coins, bullion or gold certificate bills to the nearest bank.

And look closer, there were criminal penalties for violating that order:

$160,000 fine or 10 years’ imprisonment, or both...

This has happened once before in our history…

And now I fully expect it to happen again.

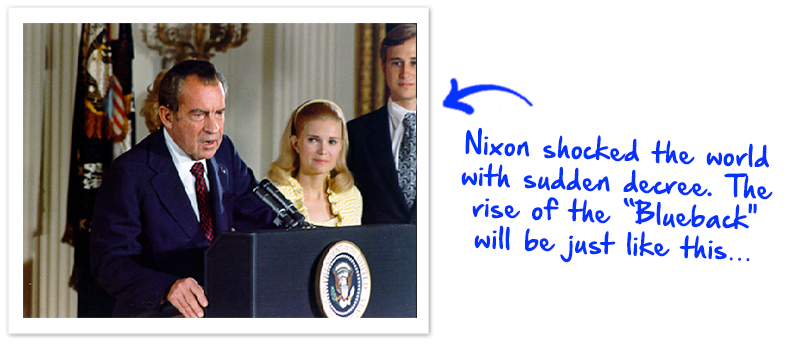

The announcement of the executive order will be like when Richard Nixon took to the airwaves on August 15, 1971, without notice to demonetize gold in America:

But this time, the government won’t go after your gold…

Instead, they will take to the airwaves…

And they’ll outlaw the physical cash you and I grew up with.

Our greenbacks will be illegal to hold.

Under penalty of jail, you’d have to report to your nearest bank branch.

If you’re lucky, you’ll be able to comply online or at an ATM that’s capable of taking cash deposits where you answer a pre-programmed questionnaire about your income, your net worth and why you have any cash in the first place.

But more likely, you’ll have to wait in line… or make an appointment… and come with a briefcase, filled with your cash, to speak face to face with a human being.

As you approach the bank teller’s counter, a government-approved agent with cold, lifeless eyes asks you to unzip your case, and present the cash.

He “politely” asks you to fill out a Currency Transaction Report with your name, where you live, an outline of your net worth, and your Social Security number and to give him the reason you even have cash in the first place...

From the way he’s dressed — in black military fatigue pants and jackboots, with a weapon on his hip — you’re certain you’ll be read your rights…

And why not? You’re a “suspicious character.”

It doesn’t matter if it’s just your emergency cash…

They'll have questions about who you are… what you do… why you have that money.

Depending on your answers, that wealth might be outright confiscated.

If you think that’s scare mongering, just google “Civil Asset Forfeiture.”

It’s the government’s technical name for their spree of cash confiscation ALREADY underway in America today.

This is where government takes your cash solely on the basis of suspicion… and it’s up to you to prove your innocence at your own cost.

Again, this is ALREADY happening in the United States of America today.

According to The Washington Post, the police have already confiscated over $5 BILLION worth of innocent Americans’ assets that went straight into the coffers of the Justice Department and the Treasury in 2014.

That was 42% more stolen cashrecorded than what actual criminals stole that year!

One poor New Jersey man had $171 confiscated for doing nothing… and needed to pay $175 to get it back!

Can you even imagine it?

Trust me, this existing trend is going to get much worse as these phases unfold.

But assuming you survive this executively ordered witch hunt, there’s...

PHASE 2: When the “Blueback” Goes Live

After everyone has deposited their cash and reported to the government on their assets, the new currency will be launched.

On an effective date, the “Blueback,” as I call it, will be declared legal tender — good for all debts, public and private.

Meanwhile, the old greenbacks will no longer be legal tender. They'll be worthless.

Why “Blueback”?

Well, it could be some other color for all we know. But the government seems to like blue ink and blue “security ribbons,” as they’re known.

Both are anti-counterfeiting security measures.

Now, look at it today:

Drastic difference, no? In composition and color. It’s blue.

The $100 bill would be the test run for this new “Blueback” that I’m anticipating.

No one knows exactly what this “Blueback” will look like, but there have been clues given by former Treasury Secretary Jacob Lew…

He’s announced a redesign of the nation's lower-denomination bills to include portraits of our great women suffragists.

Here’s one artist’s rendition of a new “Blueback” bill based on the limited information we have:

But you’re probably wondering…

Why would the government go through all of the trouble of printing a whole new currency… after they just ended the previous one?

Because once Americans’ wealth is all rounded up in the banks… and the new “Blueback” is live…

The third and most important phase will be announced...

PHASE 3: The New $:$ Exchange Rate Is Set

With no cash outstanding, a new “dollar-to-dollar exchange rate” will be announced.

The rate would be between the two different dollars:

- The new physical “Blueback” dollars…

- And digital dollars, which are electronic and in your bank account.

This sort of thing exists right now...

There’s an exchange rate between digital dollars and physical dollars… just like there’s an exchange rate between dollars and euros when you’re in the airport in Paris.

The dollar-to-dollar exchange rate is 1:1.

Think about it for a second...

If you try to withdraw $100 from your digital bank account you get — or are “exchanged” — a physical $100 bill. That’s a 1:1 exchange rate.

But after the Blueback is launched, the government will announce a NEW exchange rate between the digital dollar and the physical dollar.

And this, dear friend, is the knife that slits the fatted calf… so our blood can be drained, our skin peeled… and the government’s feast can truly begin...

Instead of 1:1… the new exchange rate might be 0.75:1.

This means if you went to your bank account and tried to withdraw $100 in Bluebacks… you’d only get $75 in physical cash.

Or, if you deposited $100 in cash into an ATM, your account balance would only add $75.

The government would literally take $25 of your hard-earned money!

This is the “Flexible Deposit Price of Paper Currency” proposal that I told you about before. The one at that monetary policy meeting in Jackson Hole, Wyoming.

Do you now see how dangerous these technical terms can really be?

In this final phase, you’re out of options.

Most people will transact digitally… either transferring money electronically, or paying only with debit and credit cards… or new payment systems like Apple Pay.

And just in case you think this sort of thing can’t happen here, you should know...

This Exact Pattern Has Happened NINE Times in American History

Over and over again throughout American history, different forms of money have been created, devalued and declared defunct.

It follows the same pattern:

- — The value of a currency evaporates

- — The government eventually announces it’s ending the currency

- — The standard of living declines

- — Eventually, future generations of Americans forget about it and have fewer ways to hold and access their wealth.

It happened in 1862 when the first fiat currency replaced the paper notes issued by private banks, giving control of money to the government.

Then, in 1862 “Demand Notes” were retired.

In 1863, the government created yet another form of money called “National Bank Notes” and made Americans use the new system by taxing their previous money up to 20% so people would switch to the new system faster. (This is just like Phase 3…)

Treasury coin notes were removed from circulation in 1899.

The turn of the century would see the Fed establish its monopoly over American currency and the removal of competing money beyond its full control…

In 1914 the Federal Reserve took control of money creation by issuing new Federal Reserve notes. More or less the ones you know today.

In 1936, gold certificates were confiscated and taken out of circulation by executive order. Any Americans that were caught in possession of the currency would be fined or imprisoned.

National bank notes were removed from circulation in 1938, leaving the Fed’s fiat money with only one competitor: silver certificates.

In 1965 the government removed all silver from quarters and half dollars. They replaced the valuable silver with worthless nickel and copper.

In 1965, the monopoly of the Fed’s fiat currency was established with the replacement of all silver certificates with the cash you know today.

And all that’s left is to retire the cash you and I have grown up with.

When?

What’s the date when we can expect the “greenback” to retire?

And when will the “Blueback” be announced and go live?

Well, I’ve pieced together the clues. And I’ve found that...

A Curious Anniversary Is Coming Up...

To be frank, I believe a plan like this could go into effect within the next 12 months.

Though no one really knows for sure — it could be put into effect much more suddenly and without warning.

Former Treasury Secretary Donald Regan put it this way in an interview with The New York Times:

“... we should quietly print new… bills… — either of a different color, or size, than the current ones. Then with only a 10-day warning, we should make all... bills… obsolete — no longer acceptable as legal tender.

Everyone would have to exchange their… bills... for new ones. Banks and other financial institutions would have to keep a record of any cash transactions over $1,000. Reports would be furnished to the… IRS by name and taxpayer identification number.”

This isn’t me talking, by the way…

Read that direct quote again…

It’s Don Regan speaking. He was an elite member of government for decades and Ronald Reagan’s Treasury secretary.

And he advocated for the following in The New York Times:

- A sudden announcement. Literally, taking Americans by surprise.

- A new colored bill.

- Retiring the old bill.

- Reporting anyone with cash over a certain limit to the IRS.

- He implied that anyone who complains or criticizes the program might be catalogued, as the IRS has already done today to political groups like the Tea Party.

Take it as proof that when a plan to steal your wealth is announced, you could have as little as ten days to get your affairs in order.

The nitty-gritty details could vary, so we’ll have to stay vigilant as more information is released.

But if I had to take a wild guess how soon this could happen…

I’d say that April 20th, 2017, could be a particularly meaningful day in this frightening paper money saga…

That’s the one-year mark since Treasury Secretary Jacob Lew announced that the $20… $10… and $5 American bills would undergo a major redesign.

At the time, the Treasury and mainstream media made a big deal out the reason why they wanted to do this redesign.

They said it was to feature more art on the currency that showed America’s history.

And they decided to add the great Harriet Tubman and other very deserving suffragists to the different bills.

But look what the Treasury’s own website says is one of the primary technical purposes of the new “Modern Money,” before aesthetics: to “maintain public confidence.”

As a lawyer, I’m trained to read every single line carefully. And I’ve been reading documents a long time…

And when I hear “maintain public confidence,” it usually means an extreme measure to stop a crisis.

Exactly what I’ve been telling you.

The problem is, the price of launching this new Blueback or something like it to “maintain public confidence” is your wealth.

The financial elites — our president, Treasury secretary, Federal Reserve chair, America’s top academics, the big bank and corporation owners…

All could be collaborating on this plan to keep our doomed financial system going.

It’s one they've been discussing for years…

It will give them total and absolute control over you and every single cent of money you have...

One that will let them freeze EVERYTHING you own… and take what they want.

Your savings account… FROZEN. (You won’t be able to withdraw anything.)

Your brokerage account… FROZEN. (You won’t be able to sell anything.)

Your retirement account… FROZEN. (All that “safe” money you thought you had will be gone.)

Your money market account… safe deposit box… bank-owned vault…

All FROZEN.

And that brings me back full circle, to the story I started this letter with…

Now it’s April 21st in our story, the day after the “Blueback” and the new dollar:dollar exchange rate went live…

Rumors of a major investment bank about to declare bankruptcy — just like Lehman Brothers in 2008 — are all over the news.

The stock market is down 5% on the headlines… then down 10%, in just a few minutes’ time…

The authorities, worried about the correction turning into a full-blown selloff and panic… decide to freeze the financial system to maintain confidence.

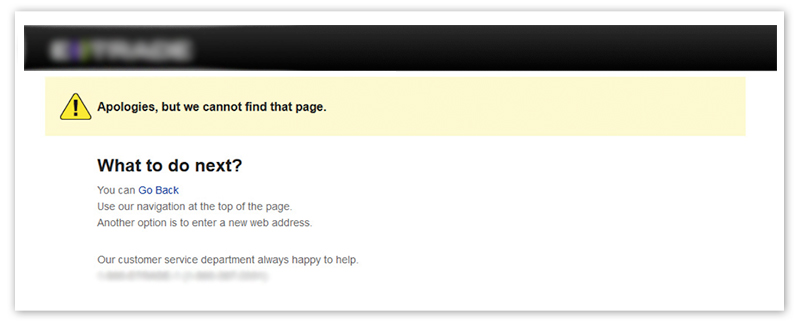

You’re worried about what’s happening, so you decide to log into your brokerage account to see how your portfolio’s fairing.

But you receive a disturbing error message...

Your heart stops for a second. You hit refresh. Same message.

It can’t be…

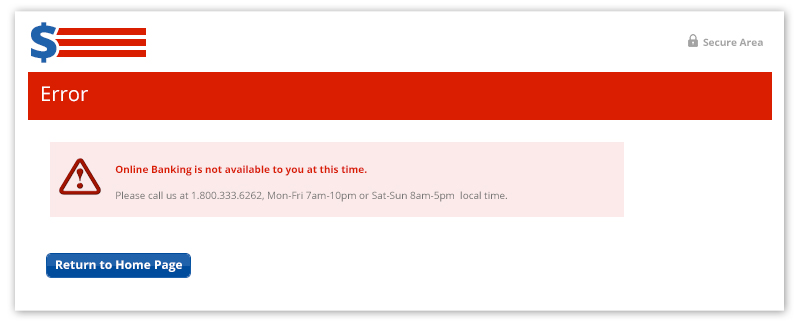

You click furiously to get over to your bank's website, and decide to log into your online bank account to see what’s happening to your money market account…

A chill comes over you — another error message.

You slam your laptop closed… and grab your jacket and car keys in one fell swoop to go down to the ATM where there’s a large angry mob, yelling.

People have been trying to make withdrawals from the ATM, but the machines are not dispensing any cash.

You push through and walk up to the machine yourself, bank card in hand.

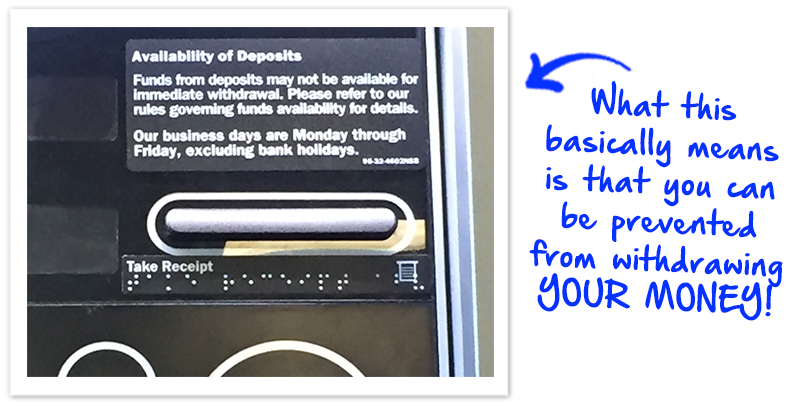

Before you even try to insert your card, you see the ATM sign that’s been staring you in face for months but you’ve never paid any attention to:

It’s only then… at the end… that you realize how helpless you are.

You should’ve done something... anything… to protect the wealth you worked so hard to build up over the years.

And the good news in all of this is: You still can.

If you’ve worked for decades and lived frugally to save your money… you still have time. But not much.

You need to take action now to protect yourself BEFORE the government exerts complete control.

That’s why I’ve prepared five steps to protect AND grow your wealth in the age of the “Blueback” & Big Brother…

These are steps I’m personally taking with more than $1,000,000 of my own money to prepare for the end of the war on cash and the launch of the government’s secret plan to steal our wealth.

So, unlike most pundits who never put their money where their mouth is, we’ll both be in thse strategies together…

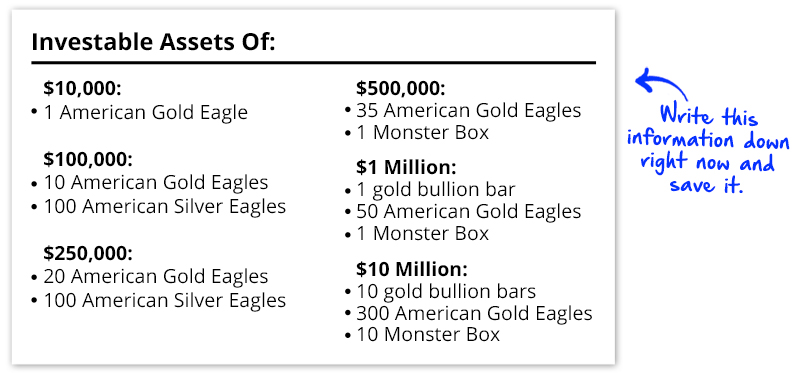

Step 1: Calculate Your Net Worth and Buy This Essential Allocation of Gold Coins...

I recommend that every single American immediately put 10% of their investable assets into gold and silver…

With the allocation to gold Eagles, Buffalos and bars in the following amounts:

But the truth is, you need to know much more information than this to successfully buy physical gold.

For example, how do you calculate your investable assets?

Do you count your house?

And who do you buy these coins and bars from?

How do you make sure you’re paying the lowest commissions?

And where do you store them?

There are a lot of questions to answer when buying physical gold — and it’s important you get it right.

That’s why I’ve put together a complete guide to answer all of these questions in a free special report that I’ve put together for you called The Perfect Gold Portfolio.

It gives you a road map for buying physical gold no matter if you’re investing $10,000 or $1,000,000.

It also includes access to my proprietary Rickards’ Precious Metals Portal, which gives you a one-click way to order and manage your precious metals.

I’ll send it to you free as soon as I hear from you today...

But you should be warned — simply protecting your wealth isn’t good enough.

Yet, I firmly believe that crises are some of the best times to MAKE MONEY, too.

That’s where the next step comes in...

Step 2: Harness the Hidden

Investment Power of DV01

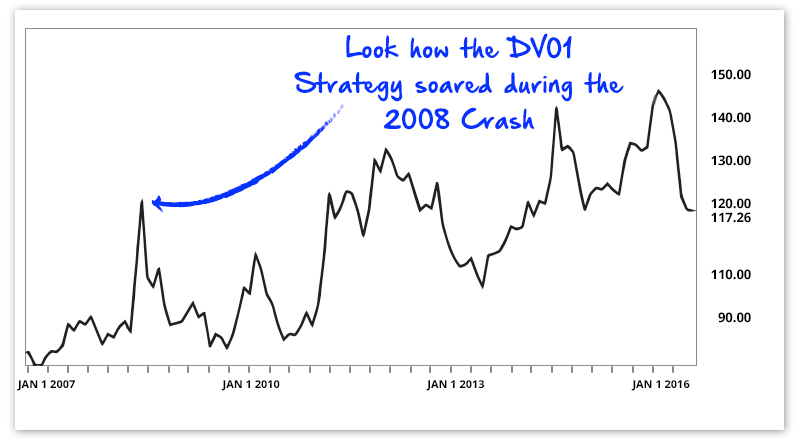

There is a simple investment strategy — not a stock, an option, a precious metal or anything you’ve considered buying before — that offers massive gains to investors in the coming crisis.

In 2008, this investment would’ve doubled your money in a short time frame — and it could’ve been purchased in your regular brokerage account.

Take a look what happened when crisis struck in 2008:

Right now, absolutely no one else that thinks the government’s too far in debt... and has printed too much money... is looking at this play right now.

It’s totally hidden…

And because of a financial phenomenon I learned firsthand after over two decades at the world's largest investment banks… something called DV01… I believe this is as certain a one-way bet as you’re handed in financial markets.

I’ll outline what this play is in a free special report called: Tap the Hidden DV01 Strategy for Potential 100% Gains.

You can get it, plus The Perfect Gold Portfolio, as soon as I hear from you.

And there’s another step you need to take if you want to be truly ready for what’s ahead…

Step 3: Buy a “Policy” From the New Secret “Government Investment Insurance Program”

If you have a bank account, you probably have heard of the FDIC — Federal Deposit Insurance Corporation.

It’s the federal government’s insurance program for all bank deposits.

All bank accounts are protected and guaranteed up to $250,000. If your bank fails… if there’s fraud… or a cyberattack… you’re protected.

Or so the government says…

The reality is much more frightening…

- For every $100 that they are on the hook to insure…

- They only have $1 to cover…

- That means $99 out of $100 of your money that you think is safe, really isn’t.

And I’ve uncovered a totally new, but little-known government program.

Believe it or not, it was my brother-in-law who tipped me off to it in 2008.

He used it to not only protect his money, but triple it when his “insurance policy” was triggered and paid out to him.

I call this new program the “SIFI Investor’s Insurance Program,” and I’ve detailed...

- What it is...

- How you can “enroll”...

- What it protects you against…

- How much a “policy” costs you…

- And under what terms it will pay out to you and in what amount…

And while all investing comes with risk and returns are not guaranteed…

- This may be one of my favorite investment ideas to share.

And I’ve detailed it in a free report briefing for you.

If I hear from you today, I’ll send it free.

I think you’ll agree after reviewing it that it’s one of the most intriguing investment situations of the 21st century, and absolutely no one else is talking about it.

And there’s more…

Step 4: Read the “Leaked” Agenda of the Financial Elites for FREE

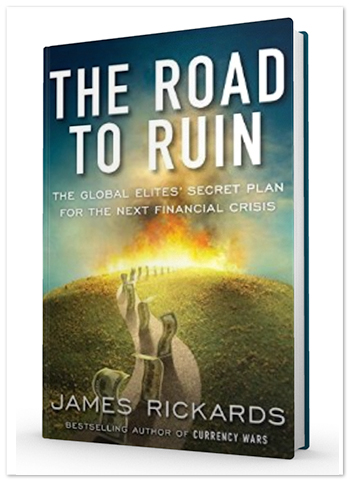

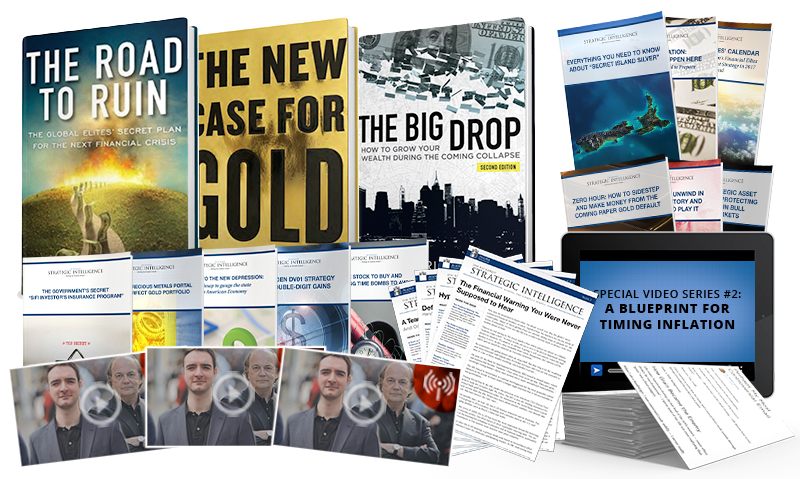

I’ve recently finished my fourth and most important book to date.

It’s called The Road to Ruin: The Global Elites’ Secret Plan for the Next Financial Crisis.

You can consider it policymakers’ and influencers’ blueprint for the next financial crisis.

I’ll ship a hard copy to your doorstep as soon as I hear from you today. Read it carefully…

This particular edition is a special printing containing bonus material that the public will not be able to buy through Amazon or Barnes & Noble.

When this book retails, it will sell for as much as $23.87. But it’s yours at no extra cost today when you answer.

You’ll learn…

- The U.S. government’s "ice-nine" plan to steal your wealth and prevent you from getting your cash. (The president, Treasury secretary and Federal Reserve chair are all colluding with world leaders to implement this plan to freeze and steal your wealth outright.) If you have a dollar to your name, you need to read page 24.

- The government doesn’t have to FORBID you to sell stocks, bonds and EFTs during the next crisis. It has a secret way to spy on you and PRESSURE you not to sell. Read all about it on page 23.

- The “Brisbane Rules” that could instantly transform any cash you have into what’s called “Forced Shares of Stock.” They're exactly that… a piece of paper you don’t want and you never asked for. (Obama approved these rules with German Chancellor Angela Merkel on November 15, 2014, with few — if any — Americans knowing about it.) Don’t let them do this to you — see page 28.

- The secret program for controlling citizens used by elites and leaders from Caesar and Napoleon to Rockefeller and Roosevelt... through both Bushes and Obama. If you think this is some conspiracy theory, you better flip to page 60 immediately, where I expose these elites by name, along with their real agenda.

- On page 61, I reveal the global elites’ shocking plan for your physical gold. (Spoiler alert: It's NOT to recreate a gold standard. Far from it.)

- My frightening finding about what’s coming for the economy and the market in 2017. The U.S. government granted me a special clearance to report on the similarities between atomic reactions and financial collapses that led me to the terrible conclusion I’m revealing publicly for the first time on page 86.

- How to inoculate yourself, your family and your wealth against the next financial crisis. If you see these happen, rest easy. The all-weather portfolio superstructure on page 297 is the most crash-proof investment strategy I’ve ever seen.

- The formula discovered in 1763 that can help you forecast the future... manage your money more profitably and even could literally save your life. I’ve shown people how to make as much as 141%, 150% and even 165% using this method. I’ve also used it to accurately predict a terrorist plot BEFORE it was thwarted by the authorities. See page 157.

- The shocking epidemic of fake gold in the West. (The Chinese have developed a new, yet little-known gold standard to protect themselves.) Please read page 162 and then check to make sure your gold is real and really will protect your wealth.

- Think runs on banks are a thing of the past? Better think again. This new, 21st-century twist on the bank run will soon leave most Americans empty-handed. Page 164.

- Why U.S. dollars are in short supply. Most Americans find this hard to believe because the Fed has printed trillions of new dollars. But the shortage is real and has serious consequences for your bank accounts and brokerage accounts. Page 164.

If you carefully read and mark up the copy I’ll send you, it will be like you're reading the most confidential plans of the world’s powerful financial elite.

The same elites that have devised and will execute this “Blueback” plan to trap your wealth in the banks…

And confiscate what they need to maintain public confidence during the next financial crisis.

Again, the book is yours free when I hear from you.

I’ve put a lot of work into all of this information for you.

But before you tell me where to send all of this information…

I need you to do something for me:

Save the Date: March 14th, 2017

I’d like to invite you to an exclusive live intelligence session on March 14th.

At the event, I will share more details about the war on cash, bail-ins and this “Blueback” plan...

I'll reveal how close the next crisis is…

Where the power elites are with their plans for you...

And I'll also be answering questions... live.

Please, just keep in mind I can’t give personalized investment advice. But I'll tell you about the latest developments in this story and how you should prepare.

Tickets to an event like this would normally cost a small fortune…

I normally charge $25,000 or more to speak at investment conferences.

But today you have the chance to join me in this live event… all free.

And that’s just the beginning of what I want to send you...

You see, as Chief Global Macro Strategist at Agora Financial — an independent forecasting firm based in Baltimore — I produce the world’s premier financial newsletter service.

It’s called Jim Rickards’ Strategic Intelligence...

From the Highest Levels of Government, Wall Street and Global Capitals to Your Inbox

Globally, over 100,000 Jim Rickards’ Strategic Intelligencesubscribers consider me their eyes and ears in the world of elite finance and politics…

My work takes me across the globe and allows me to leverage my network of high-profile contracts in Wall Street, the intelligence community and the highest levels of government.

We publish our monthly newsletter in over eight countries and four different languages.

Collectively, we spend $3 million annually to publish the boldest forecasts and information about the international monetary system… the coming crash… and steps you can take to protect and grow your wealth.

And as soon as you agree to take a trial subscription of myJim Rickards’ Strategic Intelligence newsletter today, I’ll send you…

- Report #1: The Perfect Gold Portfolio

- Report #2: Tap the Hidden DV01 Strategy for Potential 100% Gains

- Report #3: The Government’s Secret “SIFI Investor’s Insurance Program”

…Plus a special-edition hard copy of my brand-new book, The Road to Ruin,sent directly to your doorstep.

Then, each month, I’ll send you my in-depth Jim Rickards’Strategic Intelligence newsletter issue, along with updates and actionable investment recommendations.

You’ll get the first word from me on the research I gather from all of my contacts in intelligence, government and finance, and urgent news and updates on the special reports... the monthly plays... and protection strategies.

As part of my elite intelligence research service you’ll also receive:

- FREE Monthly Intelligence Briefing Webinars: Just like the briefing I’m inviting you to on March 14th, I hold these interactive briefings every month. Keep in mind, I can’t give personalized investment advice on the calls… but I can and do answer your questions about what’s about to happen in the markets and the economy.

How much does this strategic intelligence cost you?

Well, typically, the published price of a one-year subscription to Rickards’ Strategic Intelligence would run you $99 per year.

But for a short time, you can access my research advisory for just half the price of the usual rate. You'll pay only $49 for one year.

How can I manage to give my analysis and proprietary strategies for so little?

The truth is, I’m not interested in money...

I’ve spent more than a decade working to get the word out about the coming crisis. Through my best-selling books… and speeches and TV interviews... I’ve tried to warn Americans and — god willing — convince enough people to change the nation’s course.

But recently, I realize that the progress I was making was too slow. I needed to bring my strategies and continuing analysis straight to everyday Americans like you.

If you think I’m feeding you a load of bologna — here’s what I’ll do to prove to you I’m not.

Today, I’ll let you take a risk-free test drive of Rickards’ Strategic Intelligence for the next 365 days.

Over the first full year…

You can read every piece of strategic intelligence I’ve published… my monthly issues… my free reports… my live intelligence briefings and more.

That way you’ll see if my strategies… my research… and the threats to your wealth are the real deal.

Essentially, I want to take as much risk as possible away from you in order to get my research advisory service in as many Americans’ hands as possible.

If you decide for any reason my work is not right for you, just let me know and you can receive a full refund... and keep everything you've received so far.

To be clear, I’d only like you to agree to TRY Rickards’ Strategic Intelligence today with no strings attached.

I take these threats to the American economy and your wealth very seriously. I hope you’ll treat my offer today just as seriously.

I’ve given you all of the evidence. I’ve done all of the legwork and research for you. I’ve published the road map so you can protect your savings, investments and future...

Now You Have a Choice:

Digital Fiat Wealth or REAL Wealth??

You stand a crossroads.

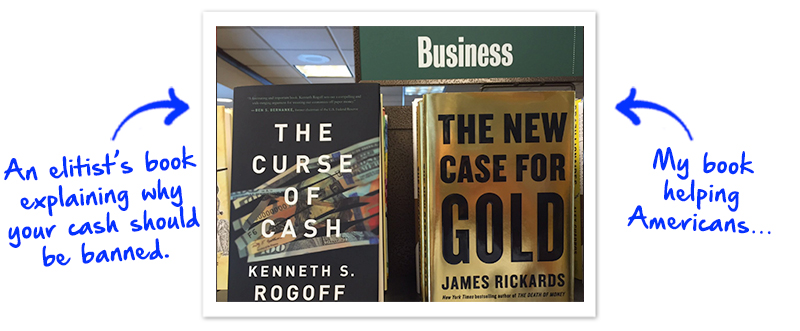

This picture I took at Barnes & Noble the other day sums it up perfectly:

On the left is elite economic policy Professor Kenneth Rogoff’s new book, The Curse of Cash. It’s about controlling your money and your life...

And on the right is my best-selling book The New Case for Gold, about real money and your financial freedom.

Which path will you choose here and now?

If you’re with Rogoff, the cash-banners and the top-downers in the Federal Reserve, good luck to you. I’m not going to send you a copy of Rogoff’s book…

But if I’ve convinced you of what’s around the corner…

And you’re ready to take action…

I hope you’ll take a trial of Jim Rickards’ Strategic Intelligence and claim everything I told you about today.

When you do, I’ll sweeten the pot by adding a hardback copy of my book, The New Case for Gold, which you see above. But only if you take advantage of my offer right here and now.

Inside you’ll learn…

- Why I trust only a handful of online bullion dealers. And why most American investors have no idea these trusted, long-standing sources exist. (Page 152.)

- The super-secret, portable asset that’s just as good as gold at storing value. Rich families have used it for centuries. And billionaires like Bill Gates and hedge fund giant Steve Cohen are using it now. (On page 169.)

- I explain why storing your gold at home could be a huge mistake. You don’t want to trust banks or storage units either. The safest option for regular gold holders is the one I name on page 154.

- The #1 gold-buying mistake investors make. You should never EVER buy gold this way... or you’ll put your finances and yourself at serious risk. (Page 165.)

And much more…

I've poured years of research into writing The New Case for Gold.

I’ve also included a special bonus chapter for you that the general public will never see. It includes five specific gold stock recommendations that won’t just protect your wealth… but grow it when the great gold hoax is exposed.

Again, I’ll send you The New Case for Gold free when I hear from you today…

Consider it my token of appreciation for being a concerned American that’s ready to take steps to protect yourself… and set an example for your neighbors.

Just say the word and give Jim Rickards’ Strategic Intelligence a try by clicking the “Subscribe Now” button below.

Clicking won’t obligate you to anything. It’ll simply take you to another page with more information.

As soon as the form is filled out, I’ll send you everything I told you about here for free.

See you on the other side...

Regards,

Jim Rickards

Febuary 2017

P.S. There’s one more thing…

As I mentioned before, I recommend that every single American put 10% of their wealth into gold and silver.

But there’s a special type of silver most people have never heard of…

I call it “Secret Island Silver.”

It’s from a tiny country near Australia and New Zealand.

The coins are minted by a major government for this secret island, and are unique because they are thick, 2 oz. silver coins.

Here’s one of the ones I own:

Now, you’ll be able to find other 2 oz. gold coins from bigger, more well-known countries like Canada or the U.S.

But they're not good walking-around money.

That’s because even though they have 2 oz., they have a wider diameter than most coins, making them very bulky to carry around.

“Secret Island Silver” solves this problem, because it has 2 oz. of silver, but the diameter is the same as a 1 oz. coin. It’s just much thicker than a normal coin.

Here, take a closer look at the side view of mine.

I don’t think you should have more than 10 or so of these coins. And they'll run you about two times the spot price of silver, plus a small premium.

A small price to pay for what they'll be worth when this Blueback plan unfolds.

I would look into getting them right now, though. And through a reputable dealer. Because I’m having trouble sourcing my own purchases right now.

And I anticipate it will be even harder, if not impossible, to get them AFTER this Blueback plan is in motion.

To help you acquire these coins, I’ve put together a report called Secret Island Silver.

Inside you’ll learn how to buy these coins… what to pay… and what to avoid from coin dealers.

Believe me, there’s NO ONE else out there talking about Secret Island Silver. But owning some will be critical for your survival in the coming years.

Click below to get started today...

P.P.S. Here’s a revised list of everything you’ll receive when you join me today. And there’s one more special gift I don’t have time to mention here. But you’ll find full details on the order page when you click the “Subscribe Now” button beneath this page.

- Free hard copy of my brand-new book The Road to Ruin: The Global Elites’ Secret Plan for the Next Financial Crisis. (This special edition will NOT be available in bookstores or on Amazon.)

- Free digital copy of The Big Drop: How to Grow Your Wealth During the Coming Collapse

- Free hard copy of my new book The New Case for Gold

- Free Report: Rickards’ Precious Metals Portal and the Perfect Gold Portfolio

- Free Report: The Government’s Secret “SIFI Investor’s Insurance Program”

- Free Report: The Hidden DV01 Strategy for Double Digit Gains

- Free Report: Everything You Need to Know About “Secret Island Silver”

- Free Report: Welcome to the New Depression: A Road Map to Gauge the State of the American Economy

- Free Report: The Global Elites’ Calendar: Secret Events of the Globe’s Financial Elites to Guide Your Investment Strategy in 2017 and Beyond

- Free Report: One Stock to Buy and 50 Ticking Time Bombs to Avoid

- Free Report: Rickards’ Strategic Asset Allocation for Protecting Your Wealth in Bull and Bear Markets

- Free Report: Zero Hour: How to Sidestep and Make Money From the Coming Paper Gold Default

- Free Report: The Great Unwind in Economic History and the #1 Way to Play It

- Free Report: Hyperinflation: It Can (Still) Happen Here and You Can Get Paid to Prepare

- Special 10-part “Essential Intelligence” Video Series

- Special Video Series #2: A Blueprint for Timing Inflation

- 24 Hours of Archived Jim Rickards’ Strategic Intelligence Audio